Commercial Property Insurance Rates: What Business Owners Need To Know

Every business needs protection. Whether you own a small café or a large warehouse, commercial property insurance helps you recover after fire, theft, storms, or other disasters. But when it comes to the cost, many business owners feel confused. Why do rates seem so different? What affects the price? And is there a way to save money without losing coverage?

Understanding these rates is not just about numbers. It’s about knowing how insurance companies see your property, what risks they focus on, and how you can make smarter choices. Let’s break down the key factors, show real examples, and give practical advice so you can control your insurance costs and avoid common mistakes.

What Is Commercial Property Insurance?

Commercial property insurance is a policy that protects your business location, assets, and equipment from damage or loss. It covers buildings, inventory, furniture, machinery, and sometimes even signs or landscaping. If your property is damaged by fire, storms, vandalism, or certain accidents, insurance helps pay for repairs or replacement.

Most policies also cover business interruption. If you must close after a disaster, insurance can help cover lost income and ongoing costs like rent or payroll.

How Are Commercial Property Insurance Rates Calculated?

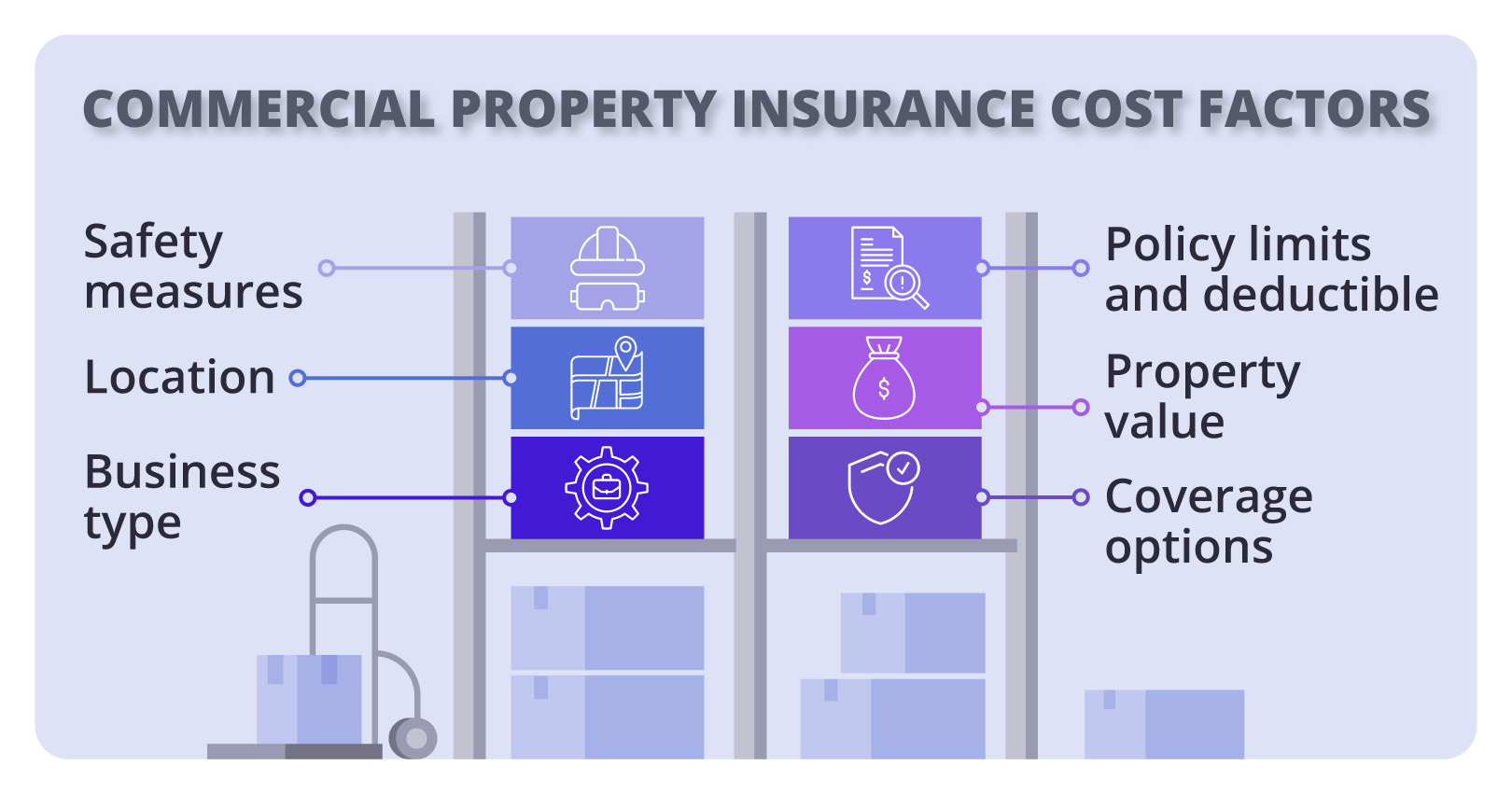

Insurance rates are not fixed. They change based on many factors, and sometimes the difference is huge—even for similar properties. Insurers use data, risk models, and experience to set prices. Here are the main elements:

1. Property Location

Where your business is located is one of the biggest factors. Areas with high crime, frequent natural disasters, or older infrastructure usually have higher rates.

| City | Average Annual Rate | Risk Factor |

|---|---|---|

| Los Angeles, CA | $4,800 | Earthquake, wildfire |

| Houston, TX | $4,200 | Flood, hurricane |

| Chicago, IL | $3,600 | Theft, winter storms |

| Phoenix, AZ | $3,000 | Heat, wildfire |

2. Building Age And Condition

Newer buildings with updated wiring, plumbing, and safety features often cost less to insure. Older structures may have hidden risks, leading to higher rates.

3. Property Value

The more expensive your property and contents, the more it costs to protect. Insurers look at replacement cost (what it costs to rebuild) and actual cash value (current value minus depreciation).

4. Type Of Business

Some businesses are riskier than others. For example, a restaurant with open flames and cooking equipment faces more hazards than a quiet office. Insurers set rates based on industry risk.

5. Security Measures

If you have alarms, cameras, fire sprinklers, and good lighting, your rates may drop. Insurers reward businesses that reduce risks.

6. Claims History

Frequent past claims can increase your premium. A clean record shows you are careful and may lead to discounts.

7. Deductible Amount

A higher deductible (the amount you pay before insurance starts) usually means a lower premium. But you must be able to handle the out-of-pocket costs if disaster strikes.

Credit: domrisk.com

Average Rates And What They Mean

Commercial property insurance costs vary. In the US, typical annual premiums range from $1,000 to $6,000 for small to mid-sized businesses. But large properties or high-risk industries may pay much more.

Let’s look at a comparison:

| Business Type | Building Value | Annual Premium | Notes |

|---|---|---|---|

| Retail Store | $500,000 | $2,500 | Low crime area |

| Restaurant | $700,000 | $4,800 | Fire risk, busy location |

| Warehouse | $1,200,000 | $6,000 | Flood zone |

| Office | $350,000 | $1,800 | Updated security |

These numbers are averages. Your actual rate depends on your details, but this gives you a rough idea.

Key Factors You Can Control

Many business owners think rates are fixed. But you can influence your premium. Here’s how:

Improve Security

- Install modern fire alarms and sprinkler systems.

- Add security cameras and motion-sensor lighting.

- Use strong locks and secure windows.

Maintain Your Property

- Fix leaks, cracks, and electrical problems quickly.

- Keep your building up to date with local codes.

- Remove clutter and flammable materials.

Choose The Right Deductible

Pick a deductible that balances risk and savings. If you can afford a higher deductible, your premium drops—but make sure it won’t strain your budget if you need to file a claim.

Review Coverage Regularly

Update your policy as your business grows. If you add new equipment or renovate, make sure your coverage matches. Over-insuring costs more, but under-insuring leaves you exposed.

Shop Around

Get quotes from several insurers. Some specialize in certain industries or regions and may offer better rates. Compare coverage, not just price.

Credit: origininvestments.com

Non-obvious Insights That Help Lower Rates

Most guides mention basics, but here are two things beginners often overlook:

- Bundling Policies: Many insurers offer discounts if you combine property insurance with liability, auto, or workers’ comp. This can save up to 15%, but only if coverage fits your needs.

- Risk Management Training: If your staff completes certified fire safety or security training, some insurers reduce your premium. This is rarely advertised but can make a real difference.

Common Mistakes When Buying Commercial Property Insurance

Even experienced owners make errors that cost money or leave them exposed. Watch out for these:

- Underestimating Replacement Costs: Many people insure for what they paid, not what it costs to rebuild today. Construction costs rise, so always check current values.

- Ignoring Local Risks: Floods, earthquakes, or storms may not be covered in standard policies. Ask about extra protection if your area faces these hazards.

- Skipping Business Interruption Coverage: It’s tempting to cut this to save money, but most businesses can’t survive weeks without income. It’s worth the cost.

- Not Reading the Fine Print: Policies often have exclusions—like mold, wear and tear, or certain types of theft. Always check what’s not covered.

- Letting Coverage Lapse: If you forget to renew or miss payments, you may not be protected when disaster strikes. Set reminders and keep your policy active.

Comparing Commercial Property Insurance Providers

Different insurance companies focus on different needs. Some work with small businesses, while others handle large properties. Here is a comparison of three well-known US providers:

| Provider | Target Business Size | Special Features | Customer Satisfaction |

|---|---|---|---|

| Nationwide | Small to medium | Bundle discounts, flexible policies | 4.2/5 |

| Chubb | Medium to large | High-value coverage, global support | 4.5/5 |

| Travelers | All sizes | Strong claims process, risk consulting | 4.0/5 |

Always check reviews, financial strength, and response times before choosing a provider.

How To Get An Accurate Quote

To get the best rate and coverage, prepare this information:

- Your business address and type

- Detailed description of your property and assets

- Current safety and security features

- Past claims history

- Desired deductible and coverage limits

Share clear and honest details. Insurers may check your history and inspect your property, so accuracy matters.

Real Example: Small Business Owner’s Insurance Rate Journey

Maria runs a bakery in Dallas, Texas. Her first quote was $4,200 per year. After installing a fire alarm, upgrading locks, and increasing her deductible from $1,000 to $2,500, her premium dropped to $3,400. She also bundled property insurance with liability coverage, saving another $300.

This shows that small changes can make a big difference. Always ask your insurer about discounts for safety improvements or bundled policies.

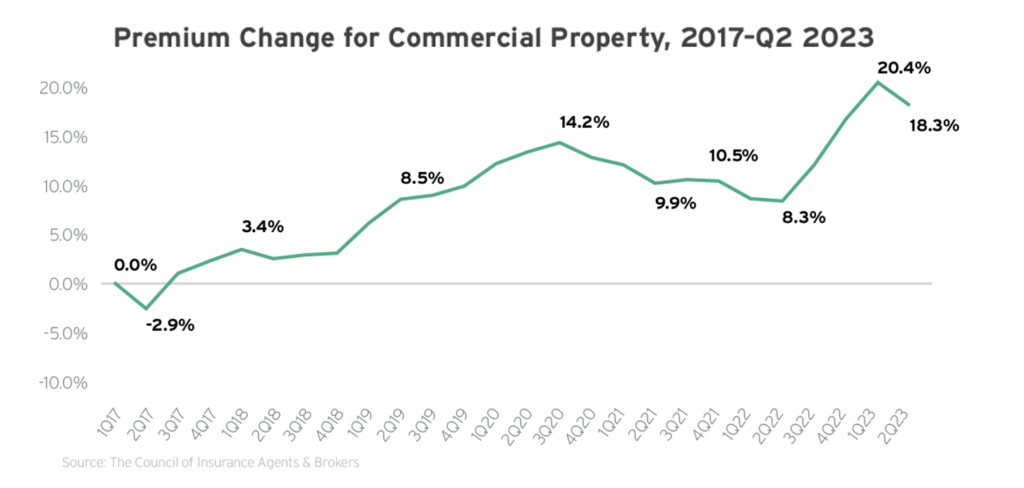

The Impact Of Natural Disasters On Rates

In recent years, disasters like hurricanes and wildfires have pushed rates higher. Insurers review local risks often and adjust prices as needed. Properties in flood or wildfire zones may see rates rise 20–30% after major events.

If your area is prone to disasters, consider extra coverage like flood or earthquake insurance. Standard commercial property policies may not cover these, so ask your agent directly.

Saving Money Without Cutting Coverage

It’s tempting to lower coverage to save money, but this can leave you exposed. Instead, focus on these steps:

- Improve safety features.

- Bundle policies.

- Keep a clean claims history.

- Compare providers yearly.

- Choose a deductible you can afford.

Never sacrifice protection for price. Losing your business is far more expensive than paying for insurance.

Frequently Asked Questions

What Does Commercial Property Insurance Usually Cover?

Commercial property insurance covers your building, equipment, inventory, and sometimes signage or landscaping. It protects against fire, storms, theft, and vandalism. Many policies also include business interruption coverage for lost income after a disaster.

How Can I Lower My Commercial Property Insurance Rates?

You can lower rates by improving security, keeping your property well maintained, choosing a higher deductible, bundling policies, and keeping a clean claims history. Training staff in safety and comparing quotes from different providers also helps.

Are Natural Disasters Like Floods And Earthquakes Covered?

Usually, standard policies do not cover floods or earthquakes. You need to buy separate coverage for these risks. Always check with your insurer and ask about local hazards.

What Happens If I Under-insure My Property?

If you insure your property for less than its replacement cost, you may not get enough money after a disaster. Insurers often pay based on actual coverage, not total loss. Always insure for current rebuilding costs.

How Do I Choose The Right Insurance Provider?

Compare providers based on coverage options, customer reviews, claims process, and price. Ask about discounts, special features, and response times. Consider their experience in your industry and local area.

If you want more details, you can read extra guidance at Insurance Information Institute.

Running a business means facing risks, but with the right insurance, you protect your property, income, and future. Take time to understand your options, ask questions, and make improvements. Smart decisions today can save you money and trouble tomorrow.

Credit: www.insureon.com

Read More:

- RV Insurance Coverage Comparison: Find the Best Plan for You

- Mortgage Protection Insurance Policy: Essential Guide for Homeowners

- Event Liability Insurance Coverage: Protect Your Next Event Now

- Insurance Lead Generation Services: Boost Your Sales Fast

- Gap Insurance for Financed Cars: Protect Your Investment Today

- Best Auto Insurance for Veterans: Top Discounts and Coverage

- Vision Insurance Plans for Families: Protect Your Loved Ones’ Sight

- Online Insurance Broker Platforms: Simplify Your Policy Search