Buying a home is one of the biggest steps in life. It comes with excitement, but also responsibility. For most people, a mortgage is the only way to own a house. But what happens if you lose your income or something unexpected happens? That’s where mortgage protection insurance comes in. Many homeowners are unsure if they need it, how it works, or if it’s worth the money. In this article, you’ll learn exactly what a mortgage protection insurance policy is, how it works, and if it’s the right choice for you. You’ll also see real-life examples, comparisons, and practical tips that help you make a smart decision.

What Is Mortgage Protection Insurance?

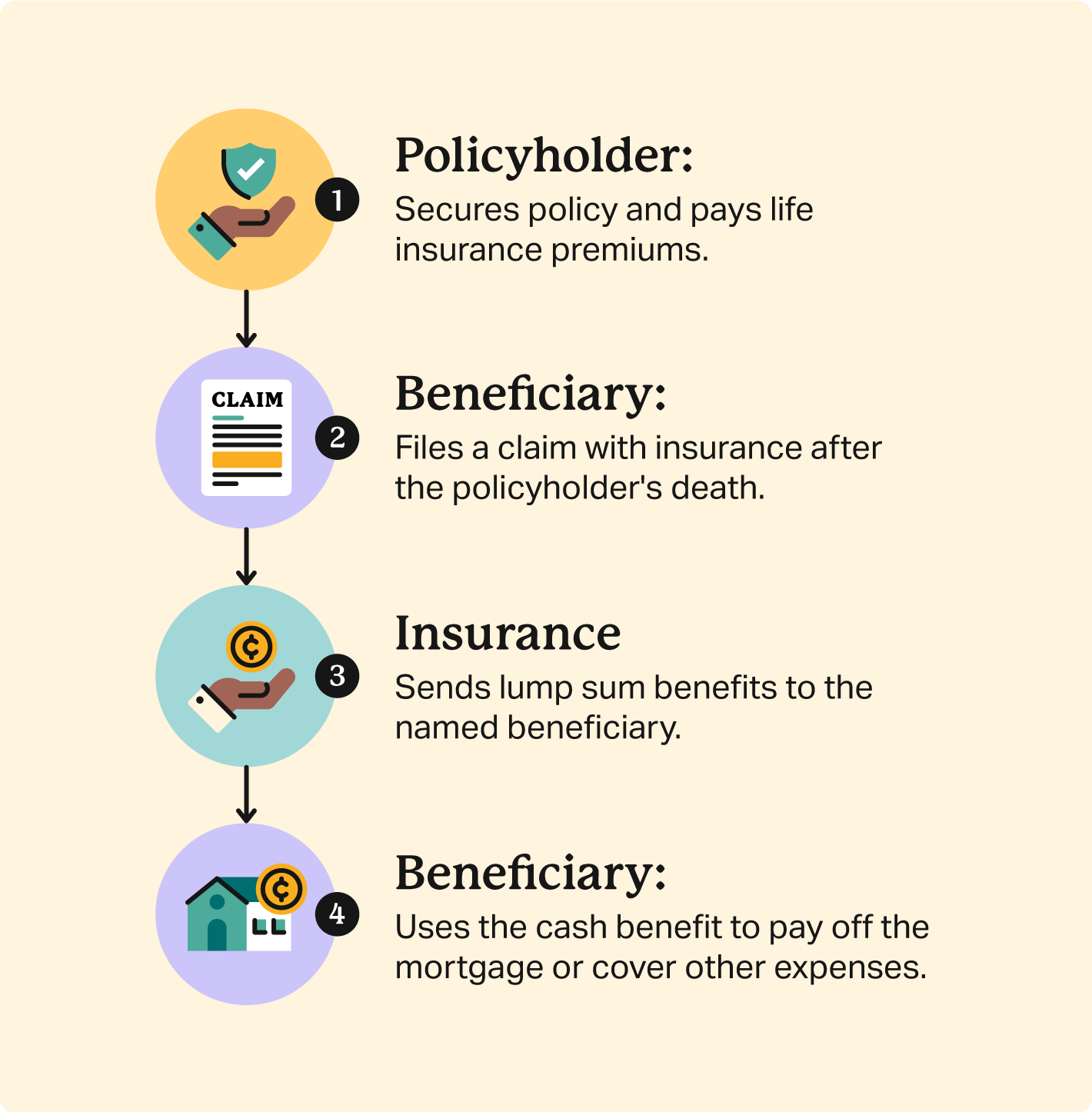

Mortgage protection insurance (often called MPI) is a special type of life insurance. Its main purpose is to pay off your mortgage if you die, become seriously ill, or lose your job. This means your family will not lose their home if you are suddenly unable to pay the mortgage.

How It Differs From Other Insurance

Some people confuse mortgage protection insurance with private mortgage insurance (PMI) or regular life insurance. Here’s a simple comparison:

- Mortgage protection insurance: Pays your mortgage if you die or face certain hardships.

- Private mortgage insurance (PMI): Protects the lender, not you, if you stop paying your loan.

- Life insurance: Pays your chosen beneficiaries a set amount when you die, which they can use for anything.

Key difference: Mortgage protection insurance is directly tied to your mortgage balance and lender. It does not usually pay your family cash, but pays the lender directly.

How Mortgage Protection Insurance Works

When you buy mortgage protection insurance, you pay a monthly premium. The policy is usually for the same length as your mortgage—often 15, 20, or 30 years. If you pass away during that time, the insurance company pays off the remaining mortgage balance.

Typical Policy Features

- Term-based: Policy lasts as long as your mortgage.

- Decreasing benefit: As you pay down your mortgage, the insurance payout decreases.

- Direct payout: The benefit goes directly to the lender, not your family.

Common Types Of Coverage

- Death only: Pays off the mortgage if you die.

- Death and disability: Pays off the mortgage if you die or become totally disabled.

- Death, disability, and unemployment: Also covers involuntary job loss for a short period.

Some policies even cover critical illnesses like cancer or heart attack, but these usually cost more.

Credit: choicemutual.com

Who Should Consider Mortgage Protection Insurance?

Not every homeowner needs mortgage protection insurance. It’s most helpful for people who:

- Have a large mortgage balance relative to their savings

- Worry their family would struggle to pay the mortgage alone

- Don’t have enough life insurance to cover the home loan

- Are self-employed or have jobs with unstable income

- Have health issues that make regular life insurance expensive or hard to get

Non-obvious insight: If you already have a solid life insurance policy, you might not need separate mortgage protection insurance. But if you can’t qualify for life insurance due to health or age, mortgage protection might still be available.

Pros And Cons Of Mortgage Protection Insurance

Understanding the real benefits and drawbacks is key before making a decision. Here’s a quick look:

| Pros | Cons |

|---|---|

| Peace of mind for your family | Can be expensive compared to life insurance |

| No medical exam required for many policies | Payout goes to lender, not your family |

| Covers specific mortgage debt | Benefit decreases as you pay off your loan |

| May cover disability or job loss | Limited flexibility compared to life insurance |

Hidden drawback: Some policies have waiting periods or exclusions for certain causes of death or disability. Read the fine print carefully.

Credit: www.annuityexpertadvice.com

How Much Does Mortgage Protection Insurance Cost?

The cost of mortgage protection insurance depends on several factors:

- Your age and health

- Mortgage amount and term length

- Type of coverage (death only, or includes disability/unemployment)

- Insurance provider

On average, a 30-year-old with a $250,000 mortgage might pay between $30 and $50 per month for a basic policy. Adding disability or critical illness coverage can raise the premium.

Cost Example

Let’s compare estimated monthly costs for a $250,000, 30-year mortgage for different ages:

| Age | Death Only | Death + Disability |

|---|---|---|

| 30 | $35 | $55 |

| 40 | $45 | $70 |

| 50 | $65 | $100 |

Tip: The younger and healthier you are, the cheaper your premium will be.

Mortgage Protection Insurance Vs Life Insurance

Many people wonder whether mortgage protection insurance is better than regular term life insurance. Here’s a side-by-side comparison:

| Feature | Mortgage Protection Insurance | Term Life Insurance |

|---|---|---|

| Payout recipient | Lender | Your chosen beneficiary |

| Benefit amount | Decreases with mortgage | Fixed amount |

| Medical exam needed | Often no | Usually yes |

| Coverage purpose | Mortgage debt only | Any financial need |

| Flexibility | Low | High |

Non-obvious insight: Term life insurance can be cheaper and more flexible, but some people can’t qualify due to health issues. Mortgage protection insurance can be a fallback for those cases.

How To Buy Mortgage Protection Insurance

Buying mortgage protection insurance is straightforward, but smart choices matter. Here’s a step-by-step guide:

- Check your current coverage. See if your existing life insurance is enough to cover your mortgage.

- Compare offers. Get quotes from at least three insurance companies. Look for online reviews and financial strength ratings.

- Read the policy details. Pay attention to exclusions, waiting periods, and what events are covered.

- Decide on coverage type. Choose between death only, death + disability, or additional options.

- Complete the application. You’ll share your mortgage details and basic health information. Most policies do not require a medical exam.

- Review before signing. Make sure you understand when the policy starts and stops, and who receives the payout.

Practical tip: Don’t feel pressured by your lender to buy their recommended policy. You can shop around and often find better deals.

Common Mistakes When Choosing Mortgage Protection Insurance

Making the wrong choice can cost you money and leave your family unprotected. Watch for these mistakes:

- Not comparing policies. Prices and features vary a lot. Don’t buy the first offer you see.

- Ignoring policy exclusions. Some policies don’t cover suicide, self-inflicted injuries, or certain illnesses.

- Confusing PMI with MPI. Private mortgage insurance only helps the lender if you default, not your family.

- Over-insuring. If you already have enough life insurance, you may not need mortgage protection insurance.

- Underestimating your needs. If you have other large debts, regular life insurance might offer better overall protection.

Expert warning: If your health has changed since you got your mortgage, review your coverage. You might need to update or add insurance.

When Mortgage Protection Insurance Makes Sense

There are situations where mortgage protection insurance is especially useful:

- Health issues: If you can’t get term life insurance due to health, mortgage protection insurance might still be available.

- Job insecurity: If you worry about losing your job, policies with unemployment coverage can help.

- Young families: If your spouse or children couldn’t afford the mortgage alone, this policy can keep them in the home.

- Single-income households: If you’re the main earner, this policy is a safeguard.

But if you have significant savings, other life insurance, or your mortgage is almost paid off, mortgage protection insurance may not be needed.

How To File A Claim

If the worst happens, your family or estate should contact the insurance company as soon as possible. They’ll need to provide:

- The insurance policy number

- Proof of death or disability (like a death certificate or doctor’s statement)

- Mortgage details

The insurance company will review the claim and, if everything is in order, pay the remaining mortgage balance directly to the lender.

Real-life tip: Keep your policy documents in an easy-to-find place and tell your family how to access them.

Credit: www.jrcinsurancegroup.com

Real-world Example

Imagine Sarah, a 38-year-old mother with a $300,000 mortgage and two children. She doesn’t qualify for regular life insurance due to a heart condition. She buys mortgage protection insurance for $70 per month. When she unexpectedly passes away four years later, the insurance pays off her remaining mortgage.

Her children can stay in their home without financial stress.

Alternatives To Mortgage Protection Insurance

Mortgage protection insurance is not the only way to protect your home. Here are some alternatives:

- Term life insurance: Pays a lump sum to your family, who can use it for the mortgage or anything else.

- Disability insurance: Replaces part of your income if you can’t work due to illness or injury.

- Critical illness insurance: Provides a payout if you are diagnosed with a serious illness.

- Building up savings: An emergency fund can help cover mortgage payments during hard times.

Each option has pros and cons. Many financial experts recommend term life insurance for its flexibility, but the right choice depends on your needs and situation.

For more in-depth comparisons, the Consumer Financial Protection Bureau offers useful resources.

Frequently Asked Questions

What’s The Difference Between Mortgage Protection Insurance And Private Mortgage Insurance?

Mortgage protection insurance helps your family pay off the home if you die or face certain hardships. Private mortgage insurance (PMI) protects the lender if you stop paying your loan, but does not help your family.

Do I Need Mortgage Protection Insurance If I Already Have Life Insurance?

If your life insurance is enough to cover your mortgage and other needs, you may not need mortgage protection insurance. But if you want extra peace of mind or can’t get enough life insurance, it can still be useful.

Can I Cancel Mortgage Protection Insurance If I Pay Off My Mortgage Early?

Yes, you can usually cancel the policy if you pay off your home loan early. Check your contract for any cancellation fees or requirements.

Is A Medical Exam Required To Get Mortgage Protection Insurance?

Most mortgage protection insurance policies do not require a medical exam. This makes it easier for people with health issues to get coverage.

Does Mortgage Protection Insurance Cover Job Loss?

Some policies offer job loss coverage, but not all. If this is important to you, make sure your policy includes it and check for any waiting periods or limits.

Buying a home is a big commitment, and protecting it is even more important. Mortgage protection insurance is one tool that can help you keep your home safe if life takes an unexpected turn. Before deciding, compare all your options, understand the details, and make the choice that fits your family’s needs best.

With the right plan, you’ll have true peace of mind—no matter what the future brings.

Read More:

- RV Insurance Coverage Comparison: Find the Best Plan for You

- Event Liability Insurance Coverage: Protect Your Next Event Now

- Insurance Lead Generation Services: Boost Your Sales Fast

- Commercial Property Insurance Rates: What Affects Your Premiums?

- Gap Insurance for Financed Cars: Protect Your Investment Today

- Best Auto Insurance for Veterans: Top Discounts and Coverage

- Vision Insurance Plans for Families: Protect Your Loved Ones’ Sight

- Online Insurance Broker Platforms: Simplify Your Policy Search