Planning an event can be exciting, but it also comes with risks. Whether you’re organizing a wedding, business conference, concert, or charity fundraiser, unexpected incidents can happen. Someone could get injured, property might be damaged, or a vendor may fail to deliver. These situations can lead to costly lawsuits or financial losses. That’s why event liability insurance coverage is important for anyone hosting an event. In this article, you’ll learn what event liability insurance is, what it covers, how it works, and how to choose the right policy for your needs. We’ll use clear examples and real-world data so you can make confident decisions.

What Is Event Liability Insurance?

Event liability insurance is a special policy designed to protect event organizers against risks during their event. If a guest gets hurt or property is damaged, the insurance can cover legal costs, medical bills, and repair expenses. It’s often required by venues before they allow you to book the space.

The main purpose is to reduce financial stress if something goes wrong. For example, if a guest slips and falls, the insurance can pay for their medical treatment and cover any legal claims. Without coverage, the organizer might have to pay these costs out of pocket.

Event liability insurance is available for both private and public events. It’s used for weddings, birthday parties, business meetings, sports tournaments, concerts, festivals, and more. Many policies are valid just for the day of the event, while others cover multi-day or recurring events.

Why Event Liability Insurance Matters

Many people think their event will be safe, but accidents are more common than you might expect. In the US, there are thousands of injury claims each year related to events. According to the Insurance Information Institute, slip-and-fall accidents are one of the most frequent causes of lawsuits at public gatherings. Even small events can face large claims.

Here are some reasons why event liability insurance is important:

- Venue Requirements: Most venues require proof of insurance before booking.

- Legal Protection: It covers legal fees and settlements if someone sues.

- Peace of Mind: You can focus on your event without worrying about risks.

- Financial Security: It prevents unexpected costs from ruining your budget.

Even if you’re careful, accidents happen. For example, at a wedding, a guest could trip on uneven flooring. At a conference, a vendor’s equipment might damage the venue’s property. Without insurance, these incidents can become expensive problems.

What Does Event Liability Insurance Cover?

Event liability insurance usually covers two main areas:

Bodily Injury

If someone is injured during your event, the policy can pay for their medical expenses and any legal costs if they sue. Common covered incidents include slips, falls, food poisoning, or injuries caused by equipment.

Property Damage

If you or your guests damage the venue, equipment, or other property, the policy can cover repair or replacement costs. For example, if a guest spills wine on an expensive carpet or breaks a door, the insurance pays for cleaning or repairs.

Additional Coverage Options

Many insurers offer extra options, such as:

- Liquor Liability: Covers claims related to alcohol service, like injuries caused by intoxicated guests.

- Cancellation Insurance: Pays for lost deposits or expenses if the event is canceled due to reasons like weather or illness.

- Hired Equipment Coverage: Protects rented items, such as tents, audio gear, or decorations.

Some policies also cover damages caused by vendors or event staff. It’s important to review your policy and understand what’s included.

What’s Not Covered?

Event liability insurance does not cover every risk. Typical exclusions include:

- Intentional Acts: Deliberate harm or damage is not covered.

- Known Hazards: If you know about a safety issue and ignore it, claims may be denied.

- Professional Services: Injuries caused by hired professionals (like caterers) may need separate insurance.

- Automobile Accidents: Vehicle-related incidents are usually excluded.

Understanding exclusions helps you avoid surprises if you need to file a claim.

Credit: www.cambriacsd.org

Types Of Events Covered

Most policies are flexible and can cover a wide range of events. Here are some common examples:

| Event Type | Typical Risks | Coverage Needed |

|---|---|---|

| Wedding | Injury, property damage, alcohol-related incidents | General liability, liquor liability |

| Business Conference | Slip-and-fall, equipment damage | General liability, equipment coverage |

| Concert | Crowd injuries, venue damage | General liability, cancellation |

| Birthday Party | Minor injuries, property damage | General liability |

| Charity Fundraiser | Food poisoning, slips, theft | General liability, cancellation |

Some insurers may exclude high-risk events, like fireworks displays or sporting tournaments. Always check with the provider before buying.

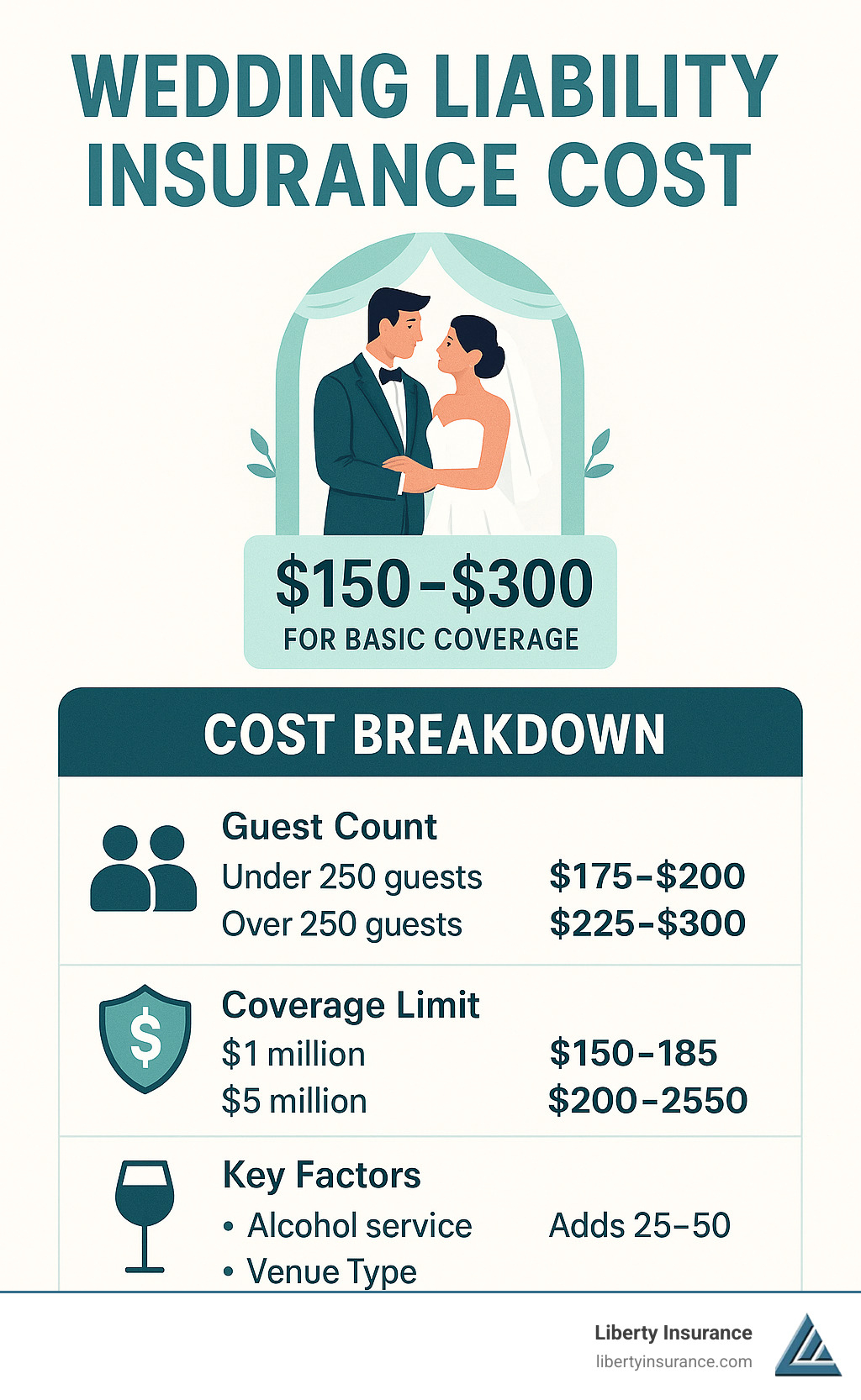

How Much Does Event Liability Insurance Cost?

The price of event liability insurance varies based on several factors:

- Type of event: Weddings and parties usually cost less than large concerts.

- Number of guests: More people means higher risk, so higher premiums.

- Coverage limits: Higher limits cost more.

- Location: Urban areas and expensive venues may increase costs.

- Duration: Multi-day events are more expensive than single-day events.

Average costs in the US:

| Event Type | Typical Cost | Coverage Limit |

|---|---|---|

| Small Wedding (100 guests) | $125 – $250 | $1 million |

| Business Conference (200 guests) | $200 – $400 | $1-2 million |

| Concert (500 guests) | $400 – $800 | $2 million |

Most policies offer coverage limits starting at $1 million per occurrence. You can increase limits for added protection, but this will raise your premium.

How To Choose The Right Event Liability Policy

Selecting the right policy can be tricky, especially for beginners. Here’s how to make a smart choice:

1. Understand Your Event’s Risks

Think about what could go wrong. Will you serve alcohol? Is it outdoors? Are there children or elderly guests? Make a list of possible hazards and match them to coverage options.

2. Compare Policy Features

Not all policies are equal. Look at:

- Coverage limits: How much will the insurer pay for each incident?

- Deductibles: What will you pay before insurance covers costs?

- Add-ons: Liquor liability, cancellation, equipment coverage.

- Exclusions: What’s not covered?

3. Check Venue Requirements

Many venues have minimum requirements. Ask for a copy and make sure your policy matches. Some venues need to be listed as “additional insured” on the policy, meaning they’re protected too.

4. Research Insurers

Choose a reputable company with good customer reviews. Some specialize in event insurance and offer tailored policies. It’s smart to get quotes from at least three providers.

5. Read The Fine Print

Don’t skip the details. Make sure you understand how to file a claim, what documents you need, and how quickly the insurer responds.

Common Mistakes When Buying Event Liability Insurance

Beginners often make costly mistakes. Here are two non-obvious pitfalls:

- Underestimating Guest Count: Many people guess the number of guests. If more people attend than planned, you could be underinsured. Always estimate generously.

- Skipping Additional Coverage: Some think basic liability is enough. But if you serve alcohol, liquor liability is crucial. Without it, alcohol-related injuries may not be covered.

Another mistake is buying insurance too late. Some policies require coverage to be purchased days or weeks before the event. Make sure to plan ahead.

Real-world Example

Let’s look at a real scenario. In 2022, a wedding in California had over 200 guests. A guest tripped over a power cord and broke their arm. The venue required event liability insurance with a $1 million limit. The policy paid for medical bills and legal costs, saving the organizer over $40,000.

Without insurance, this could have caused financial hardship.

How To File A Claim

If something goes wrong, follow these steps:

- Notify your insurer: Contact them as soon as possible.

- Gather evidence: Take photos, collect witness statements, and keep receipts.

- Fill out forms: Most insurers have claim forms you must complete.

- Cooperate: Provide all requested information quickly.

Claims are usually processed within a few weeks. If you’re unsure about a detail, ask your insurer for guidance.

Credit: libertyinsurance.com

Comparing Event Liability Insurance To Other Policies

Some people confuse event liability insurance with other types of coverage. Here’s a quick comparison:

| Policy Type | What It Covers | When Needed |

|---|---|---|

| Event Liability Insurance | Bodily injury, property damage at events | Any event with guests or rented venue |

| General Business Liability | Ongoing business risks | Regular business operations |

| Homeowners Insurance | Personal property, home-related incidents | Private parties at home |

| Cancellation Insurance | Lost deposits, canceled events | Events at risk of cancellation |

Event liability insurance is different because it’s designed for temporary risks during a specific event.

Where To Buy Event Liability Insurance

You can buy event liability insurance from many sources:

- Insurance agents: Local agents can offer advice and custom options.

- Online providers: Many companies let you buy policies online. Look for easy quote tools and clear terms.

- Specialist insurers: Some companies focus on events and can help with unusual needs.

A reliable starting point is the Insurance Information Institute, which offers detailed guides and trusted links.

Credit: www.alfainsurance.com

Frequently Asked Questions

What Is The Minimum Coverage Needed For Most Venues?

Most venues require $1 million per occurrence, but some may ask for higher limits if the event is large or risky.

How Far In Advance Should I Buy Event Liability Insurance?

It’s best to buy at least 2–4 weeks before your event. Some insurers require coverage to be in place several days ahead.

Does Event Liability Insurance Cover Covid-19 Related Cancellations?

Most policies do not cover cancellation due to pandemics unless you buy special coverage. Always check your policy for details.

Can I Add Extra Insured Parties To My Event Liability Policy?

Yes, you can usually add the venue or other partners as “additional insured” at no extra cost. This protects them as well.

Is Event Liability Insurance Required By Law?

Event liability insurance is not required by law, but many venues and cities require it before granting permits.

Making your event safe and secure is easier when you understand your risks and choose the right coverage. Event liability insurance is a simple way to protect yourself, your guests, and your investment. Take time to compare options, read the details, and plan ahead.

With the right policy, you can enjoy your event and handle surprises with confidence.

Read More:

- RV Insurance Coverage Comparison: Find the Best Plan for You

- Mortgage Protection Insurance Policy: Essential Guide for Homeowners

- Insurance Lead Generation Services: Boost Your Sales Fast

- Commercial Property Insurance Rates: What Affects Your Premiums?

- Gap Insurance for Financed Cars: Protect Your Investment Today

- Best Auto Insurance for Veterans: Top Discounts and Coverage

- Vision Insurance Plans for Families: Protect Your Loved Ones’ Sight

- Online Insurance Broker Platforms: Simplify Your Policy Search