When you buy a car with a loan, there’s a lot to think about. You want the best price, the right loan, and good insurance. But one thing many people miss is gap insurance. For financed cars, gap insurance can be a lifesaver if you have an accident or your car gets stolen. Without it, you could end up owing thousands of dollars—even after your regular insurance pays out. This article explains what gap insurance is, how it works, who really needs it, and some things most people never realize until it’s too late.

What Is Gap Insurance?

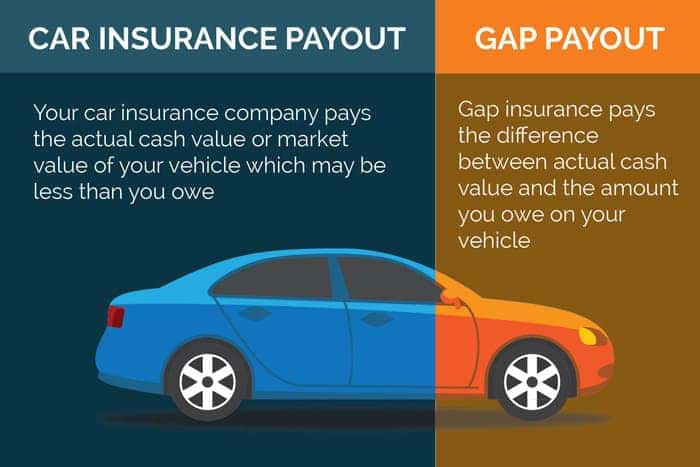

Gap insurance (short for “Guaranteed Asset Protection”) is a special type of car insurance. It covers the difference (the “gap”) between what you owe on your car loan or lease, and the car’s actual cash value if it’s totaled or stolen. Regular auto insurance usually pays the market value of your car, not what you owe on your loan.

Here’s a simple example: Imagine you buy a new car for $30,000. After a year, you still owe $27,000 on your loan, but the car’s value has dropped to $22,000. If you get into an accident and your car is declared a total loss, your regular insurance will pay $22,000 (minus your deductible). You still owe the bank $27,000, so you’re $5,000 short. Gap insurance covers that $5,000.

Why The Gap Exists

Car values drop fast—sometimes faster than you pay off your loan. This is called depreciation. New cars lose value quickly, often by 20% to 30% in the first year alone. If you made a small down payment or chose a long loan term, you might owe more than your car is worth for a long time.

Key causes of the gap:

- Low Down Payment: If you put little or no money down, your loan starts high.

- Long-Term Loans: Loans of 60, 72, or even 84 months spread payments out, but you pay off the principal slowly.

- Negative Equity: If you rolled old debt from a previous car loan into your new loan, your balance is higher than the car’s value.

- High Depreciation: Expensive cars or models with poor resale value drop in price faster.

How Gap Insurance Works

Gap insurance steps in only if your car is totaled or stolen and not recovered. It pays the lender the difference between your auto insurance payout and your remaining loan or lease balance.

Example Breakdown

Let’s see gap insurance in action:

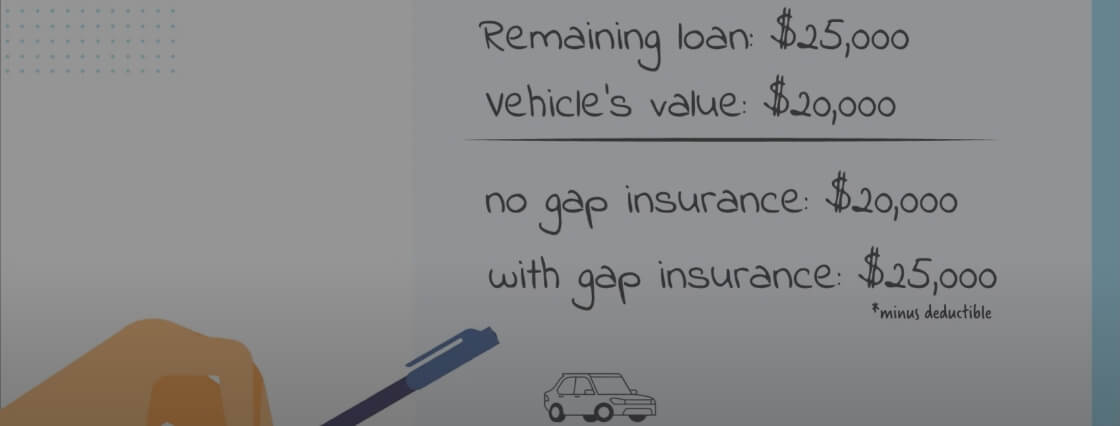

- Car purchase price: $28,000

- Loan balance when accident happens: $25,000

- Actual cash value at the time: $20,000

- Insurance payout: $20,000 (minus deductible)

- Gap: $5,000

Without gap insurance, you pay $5,000 out of pocket to settle your loan. With gap insurance, that $5,000 is covered.

What’s Not Covered

Gap insurance covers only the loan balance—not late fees, missed payments, or extra products (like extended warranties). It also doesn’t pay for repairs or for a new car. You still need comprehensive and collision coverage.

Who Needs Gap Insurance?

Not everyone needs gap insurance, but for some it’s essential. Here’s who should consider it:

- New Car Buyers: New cars lose value fastest. If you buy new, you’re at risk for a gap.

- Low Down Payment: If your down payment was less than 20%, you likely owe more than the car is worth.

- Long Loan Terms: Loans over 60 months (five years) keep you “upside down” longer.

- Leased Vehicles: Many leases require gap insurance. Leasing companies often include it in the contract.

- Rolled-Over Debt: If you added money from a previous loan, you’re more at risk.

If you buy a used car, put down a big down payment, or pay off your loan quickly, gap insurance might not be worth it.

Credit: www.eddystoyota.com

Where To Buy Gap Insurance

There are three main places you can get gap insurance:

- Dealerships: Easy, but often expensive. Dealers sometimes roll the cost into your loan, which means you pay interest on it.

- Car Insurance Companies: Often cheaper than the dealership, and you can add it to your current policy.

- Banks or Lenders: Some offer gap coverage as part of your loan, sometimes called “GAP waiver.”

Cost Comparison

Here’s how gap insurance costs compare across sources:

| Source | Typical Cost (One-Time) | Typical Cost (Per Year) |

|---|---|---|

| Dealership | $400–$800 | — |

| Insurance Company | — | $20–$40 |

| Lender | $300–$700 | — |

Buying from your insurance company is usually cheapest and lets you cancel anytime.

How Long Do You Need Gap Insurance?

Gap insurance is meant to be temporary. You need it only while your loan balance is higher than your car’s value. Once you “catch up” and owe less than the market value, you can cancel gap coverage.

How To Check If You Still Need It

- Check your loan balance: Log in to your lender’s website or check your statement.

- Find your car’s value: Use guides like Kelley Blue Book or Edmunds.

- Compare: If your loan balance is lower than your car’s value, you can safely drop gap insurance.

Some people forget to cancel gap insurance after they no longer need it, wasting money each year.

Credit: www.clearautomotivegroup.com

Common Misunderstandings About Gap Insurance

Many drivers get confused about what gap insurance does and doesn’t do. Here are a few common myths:

- “It replaces my car.” It doesn’t buy you a new car—just covers the loan gap.

- “It pays for repairs.” Gap insurance applies only when the car is totaled or stolen.

- “I have full coverage, so I’m fine.” “Full coverage” usually means liability, collision, and comprehensive—but it doesn’t cover loan gaps.

- “I must buy from the dealership.” You have choices; shop around for the best price.

Real-world Example

Let’s say Maria buys a new SUV for $35,000 with a $2,000 down payment and a 72-month loan. Two years later, her SUV is totaled in a storm. She still owes $28,000, but her insurance company values the SUV at $23,000.

Without gap insurance, she must pay $5,000 out of pocket. Because she added gap insurance for $30/year with her insurer, she pays nothing extra—the gap is covered.

How To Add Gap Insurance To Your Policy

If you already have car insurance, adding gap coverage is simple. Most major insurers offer it as an add-on. You’ll need:

- Your car’s details: Year, make, model, and VIN.

- Loan information: Lender’s name and your loan balance.

- Current policy: Check if you already have gap coverage—you might have added it and forgotten.

Call your agent or log in online. It can often be added instantly.

Is Gap Insurance Required?

Gap insurance isn’t required by law in the US, but some lenders or leasing companies may require it as a condition of your loan or lease. Always read your contract carefully. If it’s required, make sure you don’t pay twice (for example, both the dealer and your insurer).

Pros And Cons Of Gap Insurance

Here’s a quick look at the main advantages and disadvantages:

| Pros | Cons |

|---|---|

| Protects against big loan balances | Extra cost |

| Peace of mind for new or expensive cars | May not be needed for everyone |

| Prevents out-of-pocket payments if car is totaled | Dealers may overcharge |

| Easy to add and cancel | Does not cover repairs or replacement car |

Two Insights Many People Miss

- You might already have gap coverage. Some auto loans or leases automatically include gap insurance in your contract. Check your paperwork before buying extra coverage. Paying twice is a common and costly mistake.

- Cancel at the right time. Gap insurance is only valuable while you owe more than your car’s value. Many people leave it in place for years after it’s needed, wasting hundreds of dollars. Set a reminder to review your loan balance and car value every year.

Gap Insurance Vs. Loan/lease Payoff Coverage

Some insurers offer “loan/lease payoff” coverage instead of gap insurance. These are similar, but not always the same. Loan/lease payoff may only pay up to a certain percentage (like 25%) above the car’s value. Always read the fine print.

For example, if your insurer’s loan/lease coverage only pays up to 25% more than the car’s value, but your gap is bigger, you’ll be left with a bill. True gap insurance pays the full difference.

How To Make A Gap Insurance Claim

If your car is totaled or stolen, here’s what to do:

- File a claim with your regular auto insurer first.

- Get the payout amount from your insurer.

- Check your loan balance with your lender.

- Contact your gap insurer with both numbers. They’ll pay the lender directly.

- Keep all documents from both companies.

Gap insurance companies pay the lender, not you. If you had a late payment or past-due fees, you may need to pay those yourself.

Credit: www.progressive.com

Alternatives To Gap Insurance

Gap insurance isn’t the only way to avoid a loan gap. Here are some alternatives:

- Make a bigger down payment: The more you put down, the less likely you’ll owe more than the car’s value.

- Choose a shorter loan: Shorter loans cost more per month but pay off the car faster.

- Buy used instead of new: Used cars depreciate more slowly.

- Check if your credit card or loan includes gap protection: Some special offers or credit cards might include limited gap coverage.

For more details on car insurance and gap coverage, you can visit the Consumer Financial Protection Bureau.

Frequently Asked Questions

What Does Gap Insurance Cover?

Gap insurance covers the difference between your car loan or lease balance and what your regular auto insurance pays if your car is totaled or stolen. It does not cover repairs, rental cars, or new car replacement.

How Do I Know If I Need Gap Insurance?

You probably need gap insurance if you bought a new car with a small down payment, have a long loan term, or leased your vehicle. If you owe more than your car is worth, gap insurance makes sense.

Can I Cancel Gap Insurance Early?

Yes. You can cancel gap insurance as soon as your loan balance is less than your car’s value. Contact your insurer or lender, and you might get a refund for unused coverage if you paid up front.

Is Gap Insurance Included In My Auto Policy?

Not always. Some lenders or leases include it, but regular auto insurance policies do not unless you add it. Check your policy documents or ask your insurer.

How Much Does Gap Insurance Cost?

Gap insurance from an insurance company usually costs $20–$40 per year. From a dealership or lender, it’s often $400–$800 as a one-time fee. Shop around to get the best deal.

Gap insurance for financed cars is simple, but it can save you from a big financial shock. If you’re buying or leasing a car and want true peace of mind, check your loan details, car value, and consider gap insurance.

The best time to protect yourself is before you need it.

Read More:

- RV Insurance Coverage Comparison: Find the Best Plan for You

- Mortgage Protection Insurance Policy: Essential Guide for Homeowners

- Event Liability Insurance Coverage: Protect Your Next Event Now

- Insurance Lead Generation Services: Boost Your Sales Fast

- Commercial Property Insurance Rates: What Affects Your Premiums?

- Best Auto Insurance for Veterans: Top Discounts and Coverage

- Vision Insurance Plans for Families: Protect Your Loved Ones’ Sight

- Online Insurance Broker Platforms: Simplify Your Policy Search