Short-term health insurance plans are becoming more popular in the United States, especially among people in transition. These plans are designed to cover basic medical needs for a limited period, usually from a few months up to one year. For many, short-term health insurance offers a fast solution when standard health plans are unavailable or too expensive.

But before you make a decision, it’s important to understand how these plans work, what they cover, and their limitations. This article will guide you through the essentials, help you compare options, and show you how to choose wisely.

What Are Short-term Health Insurance Plans?

A short-term health insurance plan is a temporary medical insurance policy. It helps pay for unexpected health expenses, like doctor visits, emergency care, and hospital stays. These plans are not meant to replace regular health insurance. Instead, they fill gaps when you are between jobs, waiting for other coverage to start, or need a quick solution.

Most short-term health insurance policies last from 3 months to 12 months. Some states allow renewal up to 36 months, but rules vary. These plans are easier to apply for because they don’t require long paperwork or annual enrollment periods.

You can often get coverage within a day or two.

Who Should Consider Short-term Health Insurance?

Short-term health insurance is not for everyone, but it can be helpful in certain situations:

- Job transition: If you lose your job and your group health insurance ends, you may need coverage before your next job starts.

- Waiting for employer coverage: Sometimes you have to wait 30–90 days before new health insurance kicks in.

- Graduating or aging out: Young adults leaving college or turning 26 and losing parents’ coverage may need a temporary plan.

- Missed open enrollment: If you miss signing up for regular health insurance, short-term plans can fill the gap.

- Traveling or moving: People relocating to a new state or country may need short-term protection until they settle.

Short-term plans are not ideal for those with ongoing health needs, such as chronic illness or pregnancy, since many exclude these conditions.

Key Features Of Short-term Health Insurance

Short-term health insurance is different from regular health insurance in several ways. Here are the main features:

- Flexible duration: Choose coverage for 1–12 months, sometimes longer.

- Quick approval: No waiting for annual enrollment; get coverage fast.

- Lower premiums: Usually cheaper than ACA-compliant plans.

- Limited coverage: Only covers basic medical needs, not preventive care or pre-existing conditions.

- No coverage for maternity, mental health, or prescription drugs in many cases.

To make these differences clearer, see the comparison below:

| Feature | Short-Term Plan | ACA Plan |

|---|---|---|

| Duration | 1–12 months | 1 year (renewable annually) |

| Enrollment | Any time | Open enrollment period |

| Coverage | Limited | Comprehensive |

| Pre-existing Conditions | Usually excluded | Covered |

| Maternity Care | Rarely included | Included |

| Prescription Drugs | Often excluded | Included |

| Cost | Lower | Higher |

What Is Typically Covered?

Most short-term health insurance plans cover emergency care and basic medical services. Common coverage includes:

- Doctor visits

- Emergency room care

- Hospital stays

- X-rays and lab tests

- Outpatient surgery

However, coverage is limited. Many plans exclude:

- Pre-existing conditions

- Maternity care

- Mental health treatment

- Prescription drugs

- Preventive care (vaccines, screenings)

Some plans let you add extras, like prescription drug coverage, for a higher premium. Always read the policy details carefully.

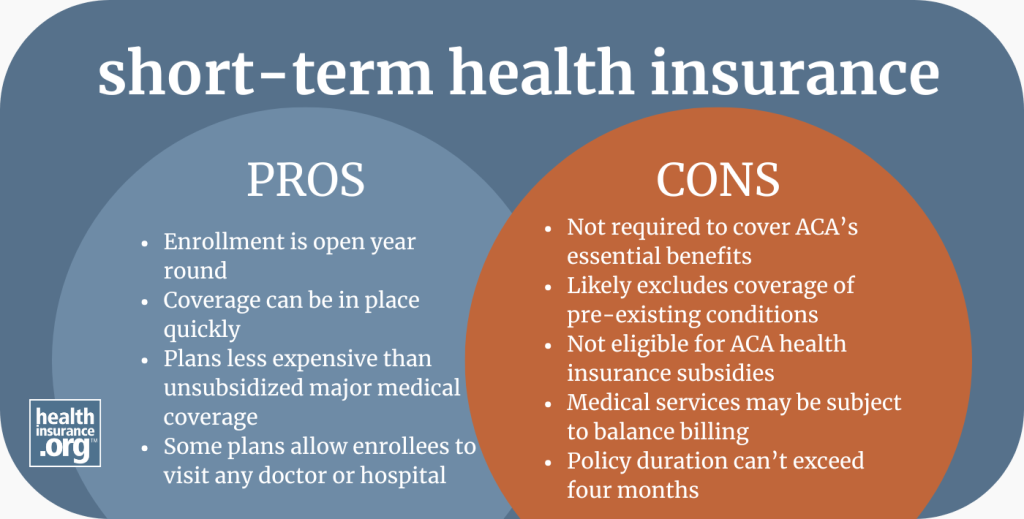

Advantages Of Short-term Health Insurance

Short-term health insurance offers several benefits for the right situation:

- Fast enrollment: Apply online, get approved quickly, and start coverage within days.

- Low monthly cost: Premiums can be up to 50% less than regular plans, making them affordable for many.

- Flexibility: Choose coverage duration to match your needs.

- Custom options: Some plans let you select extra benefits, like dental or vision.

A real-world example: After losing his job, Mike needed quick coverage for three months. He applied for a short-term plan online and was approved in 24 hours. His premium was $90 per month, much cheaper than COBRA or marketplace plans.

Disadvantages And Limitations

While short-term health insurance can be helpful, it has serious limits:

- Excludes pre-existing conditions: If you have diabetes, asthma, or other health issues, these are not covered.

- Limited benefits: No coverage for routine checkups, pregnancy, mental health, or preventive care.

- Higher out-of-pocket costs: Deductibles and coinsurance can be high, so you pay more if you need care.

- Not guaranteed renewable: If you get sick, the company may not let you renew your plan.

- No protection from ACA penalties: In states with individual mandates, you may be fined for lacking compliant coverage.

Many buyers miss these details and are surprised by denied claims or big medical bills. Always check what is excluded.

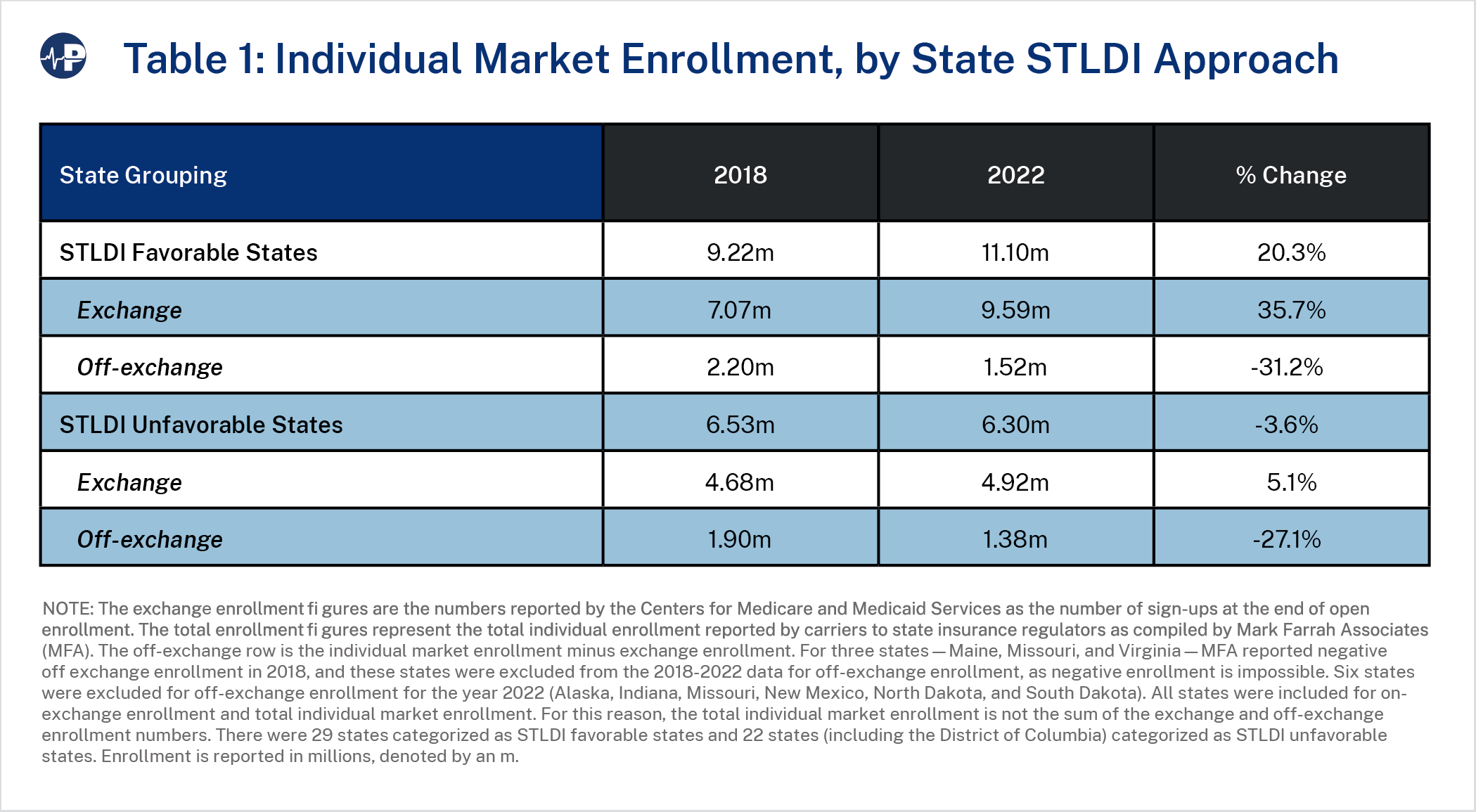

Credit: paragoninstitute.org

Cost Comparison: Short-term Vs Regular Health Insurance

Cost is often the main reason people choose short-term health insurance. Here’s a simple comparison:

| Plan Type | Monthly Premium | Deductible | Max Out-of-Pocket |

|---|---|---|---|

| Short-Term | $50–$250 | $1,000–$10,000 | $10,000–$20,000 |

| ACA Plan | $350–$600 | $500–$3,000 | $6,000–$8,700 |

Short-term plans are cheaper but carry higher risks. If you need expensive care, your costs could be much higher than with an ACA plan.

How To Choose A Short-term Health Insurance Plan

Picking the right short-term health insurance requires careful thinking. Here are steps to help:

- Review your needs: Do you only need protection for emergencies, or do you need regular care?

- Check plan exclusions: Look for what is not covered, such as pre-existing conditions or medications.

- Compare premiums and deductibles: Low premiums may come with high deductibles.

- Look for extra benefits: Some plans offer dental, vision, or prescription coverage for an extra fee.

- Understand renewal rules: Find out if you can extend your plan or if new health problems will block renewal.

A common mistake is focusing only on price. Cheap plans often have big gaps in coverage that can cost more later.

State Regulations And Legal Issues

Short-term health insurance is regulated at the state level. Some states limit plan duration or ban short-term plans altogether. For example, California and New York do not allow short-term health insurance. Other states, like Texas and Florida, permit plans up to 12 months, sometimes longer.

If you move or travel, check your new state’s rules. Coverage may not transfer, and you could lose your plan. Always ask the insurer about state restrictions before buying.

For up-to-date rules and state-specific regulations, visit the Healthcare.gov.

Non-obvious Insights Most People Miss

Many first-time buyers overlook these important facts:

- Short-term insurance does not count as minimum essential coverage under the ACA. If your state has a mandate, you may face penalties.

- If you develop a serious illness while on a short-term plan, you may not be allowed to renew or buy a new plan with coverage for that illness.

- Short-term plans often use limited provider networks. You may have to pay more for out-of-network doctors or hospitals, even in emergencies.

- Some short-term plans cap payouts for certain services. For example, a plan may pay only $2,000 for hospital stays, leaving you responsible for the rest.

Understanding these details can help avoid expensive surprises.

Credit: www.pivothealth.com

Comparing Top Short-term Health Insurance Providers

Not all short-term health insurers are the same. Here’s a quick look at some leading providers:

| Provider | Coverage Length | Prescription Option | Network Size |

|---|---|---|---|

| UnitedHealthcare | 1–12 months | Optional | Large |

| Blue Cross Blue Shield | 1–11 months | Optional | Large |

| National General | 1–12 months | Optional | Medium |

| Pivot Health | 1–12 months | Optional | Medium |

Always compare providers for network size, plan options, and customer reviews. Some insurers have better customer service and faster claims processing.

Practical Tips Before Buying

Here are some practical tips to help you make a smart decision:

- Read every policy detail before buying. Don’t rely on sales brochures.

- Ask about renewal policies. If you get sick, will you be able to renew?

- Check for hidden fees, such as application or cancellation charges.

- Make sure your preferred doctors and hospitals are in-network.

- Keep proof of coverage handy. Some states require documentation for legal purposes.

Many people regret their purchase because they didn’t read the fine print. Take your time and don’t rush your decision.

Credit: www.healthinsurance.org

Frequently Asked Questions

What Is The Maximum Duration For Short-term Health Insurance?

Most short-term plans last up to 12 months, but some states allow renewal for up to 36 months. States like California and New York do not allow short-term health insurance at all.

Are Pre-existing Conditions Covered?

No. Almost all short-term health insurance plans exclude pre-existing conditions. If you have ongoing health issues, these will not be covered.

Can I Buy Short-term Health Insurance Anytime?

Yes. You can apply for short-term health insurance at any time. There are no open enrollment periods, and coverage can start within days.

Is Short-term Health Insurance Aca-compliant?

No. Short-term health insurance does not meet ACA standards. It lacks essential benefits and protections, so it’s not considered minimum essential coverage.

What Happens If I Get Sick During My Short-term Plan?

If you develop a new illness, the plan may cover it during your current term. However, when your plan ends, you may not be able to renew with coverage for that illness. Always ask about renewal rules.

Short-term health insurance plans can be a useful tool for people in transition or facing unexpected gaps in coverage. But they come with serious risks and limits that you must understand before buying. Carefully compare options, read all policy details, and make sure the plan fits your needs.

If you need full protection or have ongoing health issues, a regular health insurance plan is usually better. Choose wisely, and protect your health and your finances.

Read More:

- RV Insurance Coverage Comparison: Find the Best Plan for You

- Mortgage Protection Insurance Policy: Essential Guide for Homeowners

- Event Liability Insurance Coverage: Protect Your Next Event Now

- Insurance Lead Generation Services: Boost Your Sales Fast

- Commercial Property Insurance Rates: What Affects Your Premiums?

- Gap Insurance for Financed Cars: Protect Your Investment Today

- Best Auto Insurance for Veterans: Top Discounts and Coverage

- Vision Insurance Plans for Families: Protect Your Loved Ones’ Sight